Spinal Implants and MIS Spinal Implants Markets to Experience Robust Growth Driven by Technological Advancements and Increased Procedural Volumes

Spinal Implants and MIS Spinal Implants Markets to Experience Robust Growth Driven by Technological Advancements and Increased Procedural Volumes

PR Newswire

VANCOUVER, BC, Oct. 2, 2024

VANCOUVER, BC, Oct. 2, 2024 /PRNewswire/ - The global spinal implants and minimally invasive spinal implants (MIS) markets are on track to experience significant growth across the U.S., Europe, and Latin America, according to the latest reports by iData Research. With a rising demand for innovative spinal surgery solutions, both markets are projected to expand, driven by advancements in minimally invasive surgical techniques and motion preservation technologies.

Spinal Implants Market

The spinal implants market is experiencing robust growth, driven by advancements across a diverse range of key segments aimed at treating various spinal conditions. This market includes vertebral compression fracture (VCF) treatments, spinal surgery instrumentation, motion preservation devices, electrical stimulation, cervical fixation, and interbody (IB) devices, all of which play a critical role in addressing spinal injuries, degenerative conditions, and deformities.

As the demand for effective spinal care continues to rise globally, innovations within these segments are enhancing patient outcomes and reducing recovery times. Motion preservation devices, for instance, offer an alternative to traditional fusion by maintaining natural spinal movement, while VCF treatments provide relief for patients with osteoporosis-related fractures. Similarly, spinal surgery instrumentation and interbody devices are evolving to support more precise and minimally invasive surgical techniques.

Shifting Spinal Implant Market Dynamics

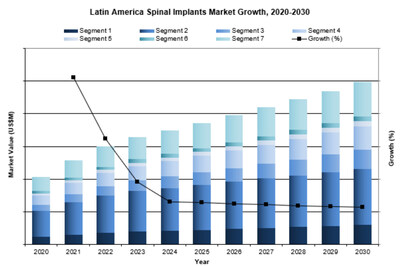

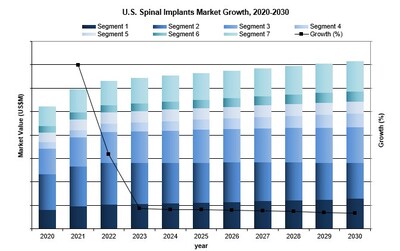

When it comes to market value, thoracolumbar fixation has long been the dominant segment in both the U.S. and Latin America, driven by its widespread use in treating a variety of spinal conditions, including degenerative disc diseases, trauma, and deformity corrections. However, this dominance is facing new challenges. Declines are expected in the coming years as certain sub-segments, such as anterior plating devices for degenerative thoracolumbar fixation, begin to slow down. The rise of motion preservation devices and minimally invasive surgery (MIS) is playing a pivotal role in this shift, offering alternatives that reduce recovery times and minimize surgical trauma, leading to a gradual shift away from traditional open surgery solutions like anterior plating.

In Latin America (Mexico, Colombia, Brazil), while thoracolumbar fixation continues to lead the market, a similar trend is emerging. The adoption of newer, less invasive technologies is accelerating. The growing acceptance of metal-based implants over traditional PEEK devices is another factor contributing to the changing market dynamics in this region, signaling a shift towards materials that offer enhanced durability and better integration with the body's natural structures.

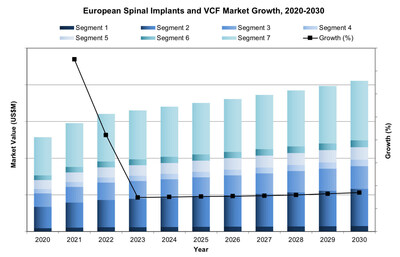

Meanwhile, in Europe, the spinal instrumentation market holds the largest market value. The steady growth of this segment is underpinned by the region's strong focus on advanced surgical techniques and increasing demand for deformity correction and trauma-related procedures. Europe's emphasis on interbody fusion and thoracolumbar fixation is expected to continue driving the market forward. Unlike the U.S. and Latin America, where declines are forecasted for certain sub-segments, Europe's spinal instrumentation market is projected to grow steadily.

The APAC spinal implant market is driven by multi-level procedures, favorable reimbursement policies, and demographic trends. In South Korea, artificial discs are replacing single-level fusion, while multi-level fusion supports growth. Favorable reimbursement in Taiwan, Japan, and Australia fosters market expansion, while China's aging population boosts demand for both fusion and non-fusion implants. These factors are shaping the market's evolution across the region.

MIS Spinal Implants Market

The minimally invasive spinal implants (MIS) market is on a remarkable growth trajectory, driven by the clear advantages that minimally invasive surgery offers over traditional open procedures. For both patients and healthcare providers, the shift to MIS is becoming increasingly appealing, thanks to its numerous benefits: reduced surgical trauma, shorter hospital stays, faster recovery times, and a lower overall risk of complications. As a result, MIS has become a game-changer in spinal surgery, particularly for patients seeking effective treatments with minimal disruption to their daily lives.

Within this rapidly evolving market, a diverse range of minimally invasive spinal implants are fueling growth. Key segments include MIS interbody devices, MIS pedicle screws, spinous process fixation, facet fixation, MIS sacroiliac joint fusion, spine endoscopes, and MIS spine instrumentation. These devices allow surgeons to perform spinal procedures through smaller incisions, thereby reducing tissue damage and leading to less postoperative pain and quicker recovery for patients. Each of these segments addresses different aspects of spinal health, offering solutions for degenerative conditions, deformities, trauma, and other spinal pathologies.

MIS Spinal Implant Markets Leading Growth

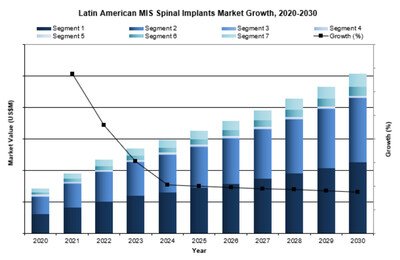

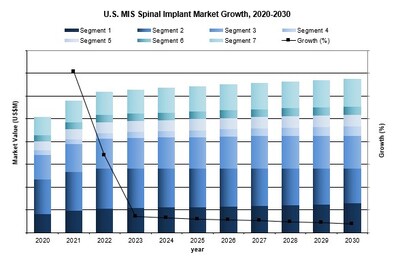

In 2023, spine endoscopy emerged as the fastest-growing segment of the MIS spinal implants market in both the U.S. and Latin America. Spine endoscopy represents a groundbreaking development in minimally invasive spinal surgery, providing surgeons with the ability to directly visualize the spinal canal. This enables the precise treatment of nerve compression, inflammation, scarring, and other spinal abnormalities with a minimal degree of invasiveness. As a result, spine endoscopy has become increasingly popular among surgeons and patients alike, offering a new frontier in spinal care. Despite its rapid growth, spine endoscopy remains a smaller segment in terms of overall procedure volume and unit sales. This is partly due to its highly specialized nature and the need for advanced training and equipment.

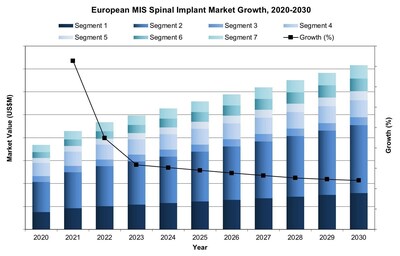

In Europe, the MIS pedicle screw market stands out as both the largest and fastest-growing segment of the minimally invasive spinal implants market. Pedicle screws are a critical component of spinal fixation procedures, providing stability and support during the healing process. The rise in percutaneous MIS pedicle screw techniques, which allow for screw placement with minimal disruption to surrounding tissues, has driven widespread acceptance of these devices in Europe. The success of MIS pedicle screws in Europe is reflective of a broader global trend. Across all regions, MIS pedicle screws account for the largest share of total minimally invasive procedural volume.

In Latin America (Mexico, Colombia, and Brazil), the MIS interbody device market is leading the way in terms of value, reflecting the region's growing demand for innovative spinal solutions. Interbody devices are used in spinal fusion procedures, where they help maintain the space between vertebrae after a damaged disc has been removed. The minimally invasive approach to interbody fusion allows surgeons to achieve the same goals as traditional surgery—stabilizing the spine and promoting bone growth—while minimizing the impact on surrounding tissues.

The MIS spinal implant market in the APAC region is driven by favorable demographics and patient preferences. In Taiwan, South Korea, Japan, and China, the aging population is boosting demand for both fusion and non-fusion procedures, with MIS fusion growing within the total fusion market. By 2030, the elderly population in these countries is expected to rise significantly, further stimulating market growth. In Australia, the increasing preference for minimally invasive procedures due to their reduced complications, quicker recovery times, and positive clinical outcomes is driving MIS unit sales, as patients favor these over traditional open surgeries.

Competitive Dynamics

The U.S. spinal implants market and the European spinal implants and MIS spinal implants markets are largely dominated by Medtronic and DePuy Synthes, two global leaders known for their extensive portfolios of spinal surgery solutions. These companies have established themselves as the top players, consistently driving innovation and maintaining a significant presence across both traditional and minimally invasive (MIS) spinal implant markets. Behind them, other key players like Stryker, ZimVie, and Globus Medical also hold substantial shares, contributing to the competitive landscape with their own advancements in spinal implant technology.

In the U.S. MIS spinal implants market, the leadership shifts slightly, with Globus Medical (which recently merged with NuVasive) and Medtronic taking the top spots. DePuy Synthes, SI-Bone, Richard Wolf, and Joimax are notable competitors in the MIS space, each bringing specialized expertise to specific niches of the market, such as sacroiliac joint fusion, endoscopic surgery, and motion preservation.

In Latin America, the competitive landscape differs slightly, with ZimVie/Highridge Medical holding the largest market share in both the traditional spinal implants and the MIS segments. DePuy Synthes, Globus Medical/NuVasive, and Medtronic also play significant roles in the region, benefiting from the increasing adoption of advanced spinal surgery techniques. Additionally, local Brazilian companies such as GMReis, Baumer, and NEOORTHO are emerging as strong contenders, leveraging their regional expertise and growing reputations to capture a substantial portion of the market.

Future Outlook

With advancements in minimally invasive surgical techniques and the growing acceptance of motion preservation devices, the spinal implants and MIS spinal implants markets are positioned for substantial growth in the coming years. As healthcare systems worldwide embrace these innovative technologies, the landscape of spinal surgery is set to evolve rapidly. For a deeper analysis of the spinal implants market, including trends, forecasts, and competitive dynamics, explore iData Research's comprehensive reports through the hyperlinks above.

About iData Research

iData Research is a leading provider of medical device market intelligence, offering comprehensive data analysis and insights across various healthcare sectors. With an established reputation for delivering accurate and actionable market research, iData helps companies navigate the evolving medical landscape to make informed business decisions.

SOURCE iData Research Inc.

-

What’s Happening in the Markets This Week

-

Worst-Performing Stock ETFs of the Quarter

-

Q3 in Review and Q4 2024 Market Outlook

-

Top-Performing Stock ETFs of the Quarter

-

September Jobs Report Forecasts Show Moderate Hiring Gains

-

Port Strike a Headache for Shippers but a Potential Tailwind for Certain US Transport Stocks

-

13 Charts on Q3′s Roller-Coaster Rally for Stocks and Bonds

-

5 Stocks to Buy Instead of Overpriced US Equities

-

Consumer Defensives: Despite Angst, Thirsty Investors Have Names to Pursue

-

Industrials: Many Stocks Overvalued After Q3 Outperformance

-

Basic Materials: Despite Index Rise, We See Multiple Long-Term Opportunities

-

What the Election Could Mean for Big Tech Stocks

-

3 Lessons From Recent Stock Market Drama

-

Consumer Cyclicals: Even Amid Moderating Consumer Spending, We See Discounts

-

Healthcare: Valuations Look Fair Overall, With Select Industries Still Undervalued

-

Utilities: Falling Interest Rates, Growth Outlook Boosting Stocks