Morningstar ranks countries’ ESG practices and assesses their levels of carbon risk.

By Valerio Baselli

ESG

By Valerio Baselli

Read Time: 4 Minutes

The outbreak of the coronavirus pandemic resulted in one of the worst quarters in history in the financial markets. In such a scenario, funds focused on buying stocks that score well on environmental, social, and governance-related metrics proved to be a safer harbor for investors.

Morningstar research shows that in the first quarter of 2020—especially in March—sustainable equity funds overall fared better than their conventional peers, and passive sustainable equity funds fared better than those following conventional market indexes.

Of course, that does not mean that ESG equity funds can escape losing money when stocks are in correction territory. Nevertheless, this latest crisis has certainly demonstrated the greater resilience of sustainable investing, as sustainable funds weathered the downturn better than their conventional peers.

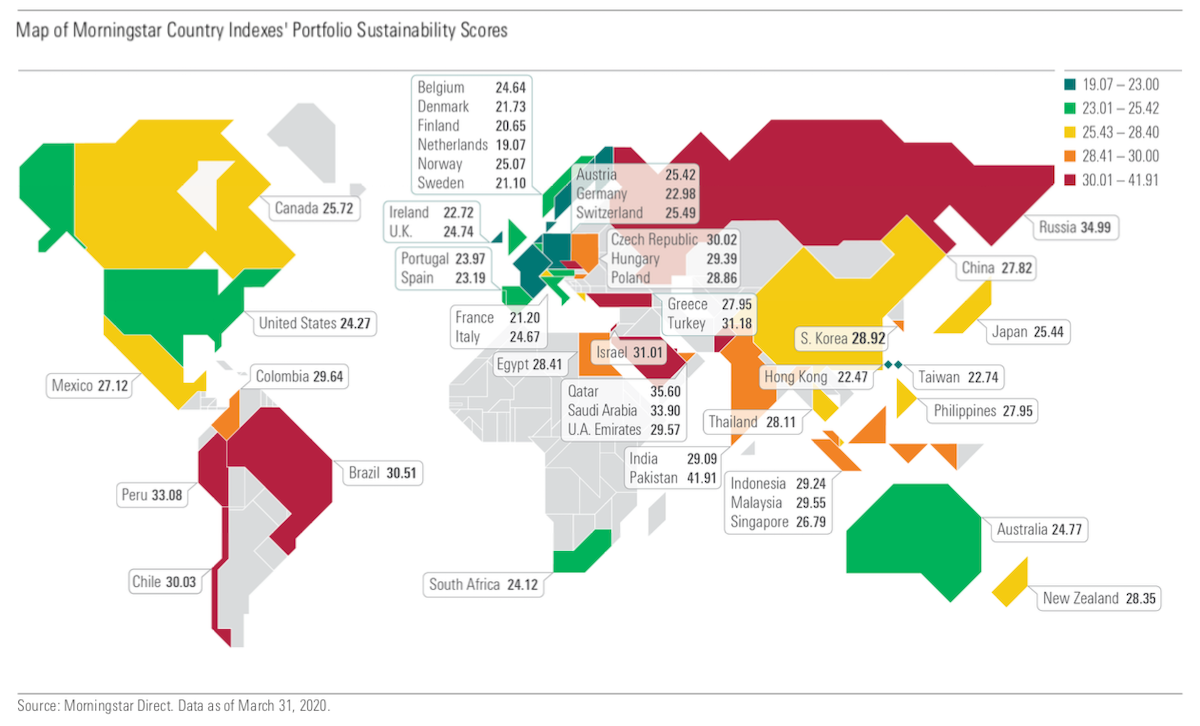

According to our latest research, European countries—particularly those in the north—lead the pack in ESG practices. This is somewhat expected, since those nations have always been ahead of the curve on this front, but a few other countries also feature exceptionally strong sustainability profiles.

Financial advisors and asset managers can use this data to identify countries with the greatest ESG investment opportunities and most significant risks.

Morningstar Sustainalytics uses the constituents of Morningstar country indexes to examine the sustainability profiles of 48 country-specific equity markets. The company-level scores are sourced from Sustainalytics, which also powers the Morningstar Sustainability Rating™ for funds.

Here, we explore some key findings about the ESG practices of countries around the world.

As in previous research, the Nordics and eurozone came out on top of sustainability rankings. Specifically, the Netherlands has the strongest overall score, followed by Finland and Sweden. Hong Kong is the world’s best-scoring non-European market for sustainability; Taiwan also lands in the first quintile in terms of sustainability.

On the other hand, several big Asian markets score poorly on sustainability: Japan and China land in the third quintile and South Korea in the fourth. And a group of Middle Eastern, Latin American, and Eastern European emerging markets, including Russia and Brazil, occupy the globe’s bottom quintile.

The full set of rankings is shown on the map below.

A few additional highlights include:

The same holds true for Italy, which ranks third on ESG Managed Risk but slips to 15th place for overall Morningstar® Portfolio Sustainability Score,™ owing the high exposure to material ESG issues involving key companies like Enel (ESOCF) and Eni (EIPAF).

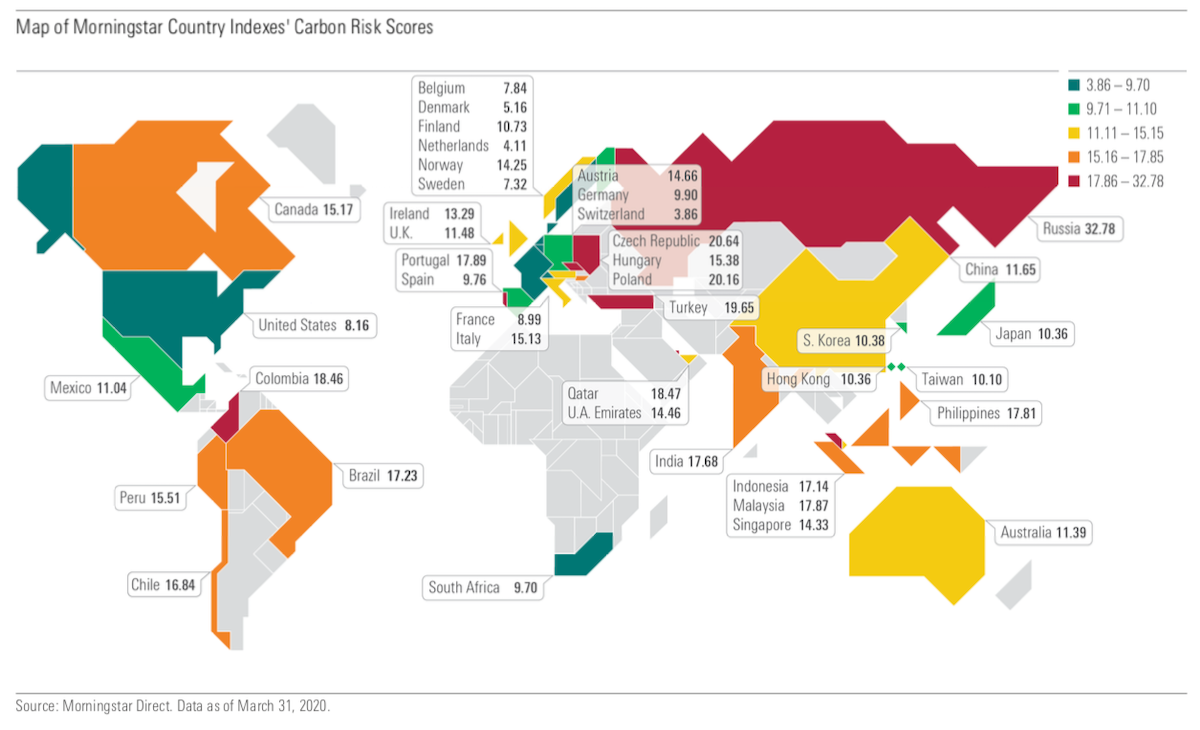

Western European markets like Switzerland, the Netherlands, Denmark, Sweden, Belgium, and France carry the lowest levels of carbon risk, as do South Africa and the U.S. The full map of scores is shown below.

Despite being the world’s second-largest carbon emitter, the U.S. has a low level of stock market value that is at risk from the transition to a low-carbon economy. This is because healthcare and technology companies represent more than 37% of U.S. equity market cap and financials stocks account for almost 14%, while energy is around just 2.5%.

On the flip side is Russia, which holds nearly 55% of its market cap in energy stocks and consequently carries the world’s highest level of carbon risk.

Financial advisors can advance the conversation about ESG material risk with clients using our robust portfolio management software. Morningstar® Office integrates ESG data, analytics, and ratings with Sustainalytics.

Disclosure

The information, data, analyses and opinions presented herein do not constitute investment advice; are provided solely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete or accurate. Past performance is not a guide to future results.

The opinions expressed are as of the date written and are subject to change without notice. Except as otherwise required by law, Morningstar shall not be responsible for any trading decisions, damages or other losses resulting from, or related to, the information, data, analyses or opinions or their use. The information contained herein is the proprietary property of Morningstar and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar.

Investment research is produced and issued by Morningstar, Inc. or subsidiaries of Morningstar, Inc. including, but not limited to, Morningstar Research Services LLC, registered with and governed by the U.S. Securities and Exchange Commission.