What Can Private Funds Offer You?

The diversification benefits are modest, but the additional risks are not.

/s3.amazonaws.com/arc-authors/morningstar/502d0355-28ed-483c-ae9d-b67bfbf5291b.jpg)

A pot of diversification gold doesn’t sit at the end of the private-market rainbow, and private investments’ structural qualities merit extra caution for individual investors. In our recently published 2024 Diversification Landscape report, Amy Arnott, Christine Benz, and I took a deep dive into how different asset classes performed in the past couple of years, how correlations have evolved, and what those changes mean for investors and financial advisors trying to build well-diversified portfolios. You can also check out Arnott’s Portfolio Basics series, where she goes over some fundamentals of assembling sound portfolios.

In contrast to most securities, which are typically traded on an exchange and valued according to rules established by the SEC, private investments involve supplying funds to a business for a dedicated period of time with the hope of (but no guarantee of) enticing future cash flows. In the case of venture capital, it means providing resources for the incubation and development of an idea into a durable business; the probability of failure is high but so, too, are the potential returns. Private equity typically refers to a more developed version of venture capital, where early-stage investment in a company that eventually goes through an IPO on a stock exchange may result in attractive upside. Private credit is when investors loan directly to companies that want to avoid the broader capital markets, typically for more favorable covenants than would be available otherwise. Leveraged buyouts, real estate, and real assets also exist under the umbrella of private investments.

And as varied as these private investments are, they share a number of structural characteristics. The first is illiquidity. Once an investment is made, those assets are committed for a significant period of time (often years) before the expectation of a return, in theory giving the management team the space that it needs to make a go of the endeavor. The second is a high barrier to entry for investors, a result of large commitment minimums and high fees relative to those of marketable public securities. The third is complex reporting. Private investments rely heavily on discretion when valuing assets, particularly in the early years when there isn’t a market precedent. An industry standard for private-company valuation is an internal rate of return. A benefit of IRRs is that they account for the time value of money—a key consideration given the longer horizons and the illiquid nature of private investing. However, there are limitations: IRRs are calculated on a delay and can be easily manipulated, rather than the clear-cut performance numbers easily derived for securities that must transparently mark to market daily.

As a whole, these defining structural characteristics mean that private investments aren’t scrutinized publicly and on a periodic schedule. Instead, they take advantage of built-in patience to give the investments the greatest probability of success. As a result, the pace and magnitude of returns differ from marketable public securities, which contributes to a perception of portfolio diversification. But in practice, many of these private investments are simply leveraged versions of existing equity and fixed-income market dynamics.

Recent Performance Trends in Private Investments

The quarterly IRRs reported by Morningstar’s PitchBook subsidiary represent the general experience of each of these private investment sectors; other indexes cited represent quarterly total returns.

In the wake of the pandemic panic (first-quarter 2020), when the Morningstar US Market Index lost 20.6%, venture capital, private equity, and secondaries (a type of investment that purchases an existing interest in a company from a private equity company) also suffered losses but at a much more modest level. Aided by their illiquid structures and delayed reporting, these results don’t as easily reflect of-the-moment market temperament in pricing. Still, as markets roared in 2021, the same investment sectors benefited from the accompanying euphoria and rock-bottom financing rates. The next two years posed more complicated dynamics for private markets: Rising interest rates, geopolitical tensions, and the banking crisis early in 2023, for example, hindered activity for some private investments and created opportunities for others. Reflected in the rolling one-year IRRs of the private capital markets, private equity, venture capital, funds of funds, and secondaries all rose sharply from early 2020, peaking in mid-2021 before starting a steep drop through late 2022. Private debt, real estate, and real assets followed a similar but less pronounced trajectory. Those asset classes’ rolling one-year IRRs grew modestly through early 2022 and then decreased at a relatively gentle slope.

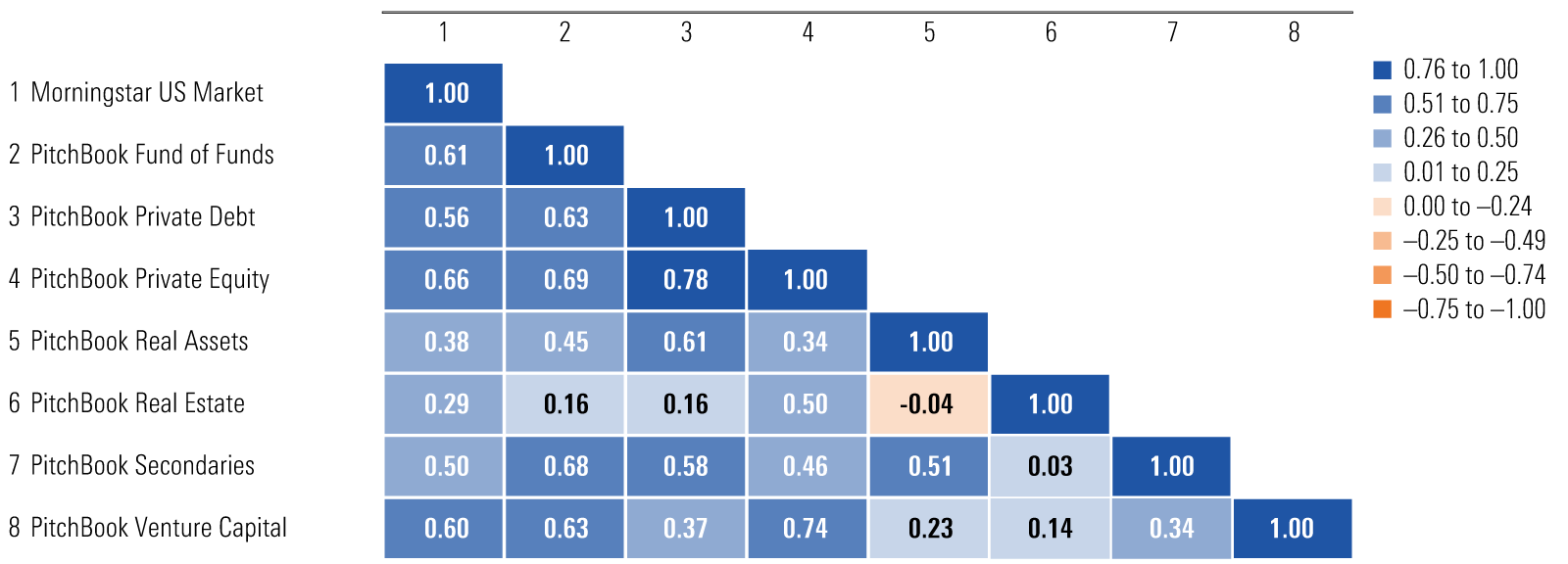

Three-Year Correlation Matrix: Private Investments

Weaker growth and higher interest rates ate into private equity’s returns in 2022 and 2023, as the cost of capital and leverage increased and market uncertainty slowed deal-making. The difficult exit environment meant that many private equity firms held on to investments that they would have otherwise sold off, slowing the flow of cash out and then back into the private capital market as investors were unwilling or unable to commit more capital.

The regional baking crisis intensified banks’ reluctance to lend in the rising-rate environment, which widened private debt’s opportunity set. As the supply of credit lines from banks slowed but demand remained high, as did interest rates, private-credit yields increased, making for a relatively favorable environment for the subasset class.

Quarterly returns for private-capital indexes (reported by PitchBook) date back to early 2000. Pricing infrequency and variability result in overly smooth results, which can obscure the volatility and correlations of private investments. To account for that, PitchBook also provides adjusted quarterly returns that better capture the investments’ volatility, facilitating more representative correlation computations. All seven private asset classes considered here exhibited a higher correlation to the broad public equity market in the past few years. The pandemic-driven drawdown, ensuing bull market, and then rising interest rates permeated through both public and private markets.

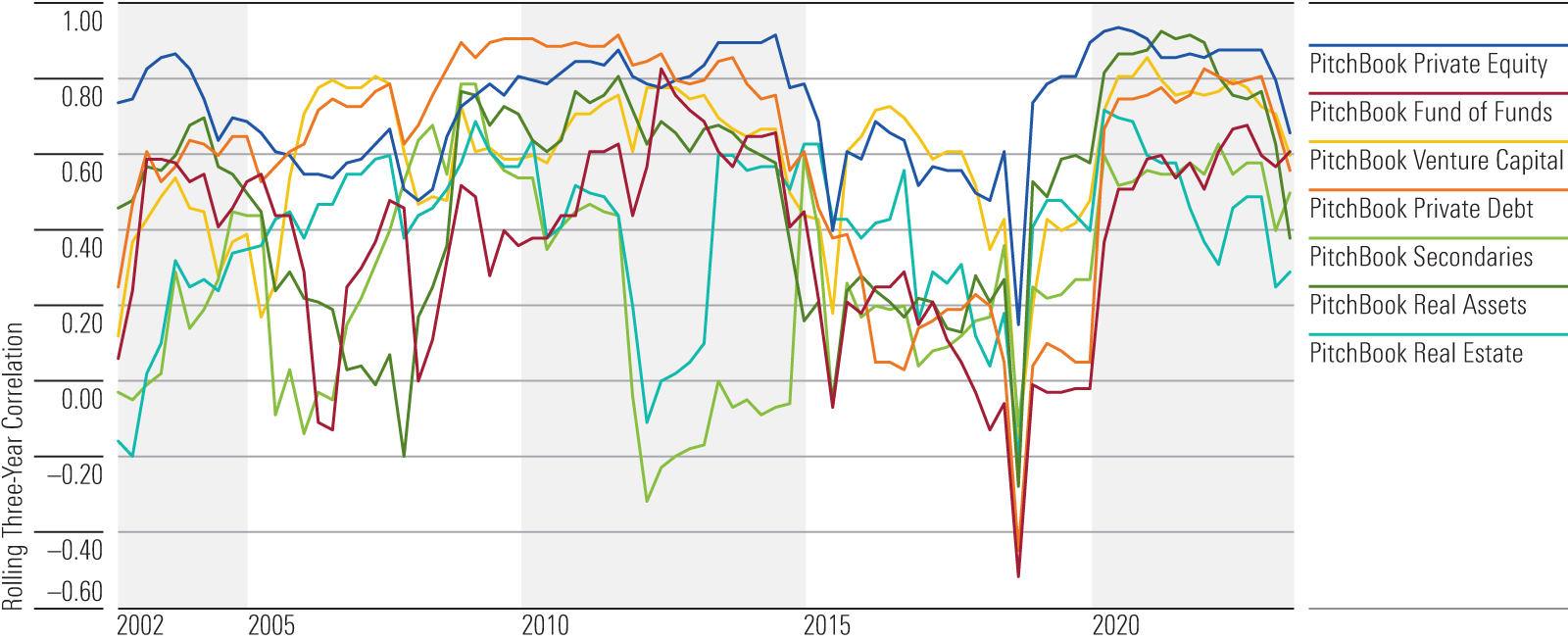

Long-Term Trends in Private Investments

The rolling three-year correlations between the private investment sectors and the Morningstar US Market Index vary widely and have also shifted dramatically over time. By definition, many of these private sectors are early-stage equities. And relative to other asset classes discussed in this paper, the range of correlations across private investments differs dramatically from quarter to quarter. Rather than reflect reality, these are somewhat products of the structural characteristics of the asset class outlined above.

Rolling Three-Year Correlations vs. Morningstar US Market Index: Private Investments

Still, within private investments, venture capital and private equity are more correlated with marketable equities than private credit, and all three of these typically exhibit higher correlations with publicly traded stocks than real assets and real estate, which are shaped by underlying factors specific to those markets. Secondaries and funds of funds exhibit the lowest long-term average correlations. Those subasset classes are sensitive to the activity of the other private asset classes, so they have a bit more distance from the public markets. However, even with that distance, secondaries’ rolling three-year correlation versus the Morningstar US Market Index has ranged from 0.79 to negative 0.32, with an average of 0.27 (measured from early 2000 to mid-2023). On the other end of the spectrum, private equity exhibited a long-term average rolling three-year correlation of 0.73, but that figure has ranged from 0.94 to 0.15, with both ends of the range occurring in the past five years.

Portfolio Implications of Private Investments

Over the long term, the structure of private investments means their cash flows will look different from those of marketable securities, which more swiftly reflect changes in market sentiment in their pricing. This enhances diversification in a theoretical way, but with such varying correlations across the private-investment subasset classes and over time, private investments may not provide consistent diversification value. Further, investors who seek private options should remain alert to the risks unique to their underlying investments. Venture capital and private equity, for example, are leveraged and concentrated equity investments by their very structure. Through longer periods, the potential for those investments is tied to many of the same factors that lift and drag on public equity markets—with amplified risk and return profiles.

While private investments remain a potential source for differentiated (though mostly delayed and leveraged) equitylike return streams, their structure merits caution for individual investors. Without access to the highest-quality endeavors with well-resourced teams to manage those projects, the investment can easily fall apart. This is potentially devastating given that the assets are committed for long periods of time with little recourse if something goes wrong. And while large institutional portfolios with unlimited time horizons and the ability to easily replenish funds may find private investments attractive, an individual investor without those benefits can more practically create diversification with other more liquid and government-regulated asset classes.

Often you have to be an accredited investor to partake, and the high investment minimums are a barrier for many individuals. If you are not an accredited investor (or if you are but don’t meet the minimum), there are some other ways to access the private capital market. For example, in the semiliquid space, interval funds and tender offer funds, both of which are closed-end funds under the Investment Act of 1940, can provide access to private investments. Still, though the asset class has garnered more attention of late, take time to understand the risks before wading into these new waters.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EC7LK4HAG4BRKAYRRDWZ2NF3TY.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/6ZMXY4RCRNEADPDWYQVTTWALWM.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/URSWZ2VN4JCXXALUUYEFYMOBIE.png)

:quality(80)/s3.amazonaws.com/arc-authors/morningstar/502d0355-28ed-483c-ae9d-b67bfbf5291b.jpg)