Key Rules for a Backdoor Roth IRA Contribution

Circumventing the Roth IRA MAGI limit is a multistep process that should be started now.

If you want to make a regular Roth IRA contribution but are disqualified because your income is too high, you can circumvent the income limit by using the backdoor contribution strategy. The backdoor contribution for a Roth IRA is a two-step process:

- Contribute to your traditional IRA.

- Convert it to your Roth IRA.

Other rules must be employed to get the intended results.

The Backdoor to the Income Restriction

Your IRA contribution is capped at the lesser of 100% of your eligible compensation for the year and the contribution limit in effect for the year. For 2024, the contribution limit is $7,000. If you are at least 50 by the end of the year, you can make an additional catch-up contribution of $1,000—making your total $8,000.

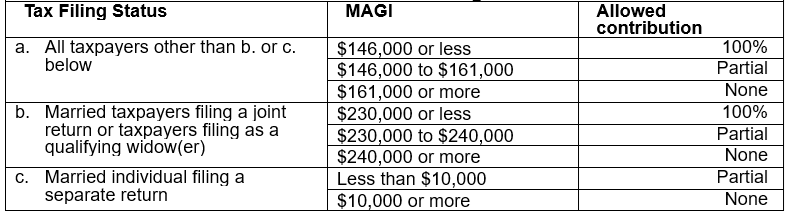

Generally, individuals can choose which of the two IRAs—traditional or Roth—to fund with their regular contribution. But unlike traditional IRAs, which allow for a regular contribution regardless of income, an individual is permitted to make a regular Roth IRA contribution only if their modified adjusted gross income, or MAGI, does not exceed certain amounts. This amount is based on tax-filing status. The following is a snapshot of the 2024 MAGI limits:

2024 MAGI Limits for Contributing to a Roth IRA

Tip: If the MAGI falls in the “partial” range, the IRA owner can contribute the eligible amount to a Roth IRA and the balance of the $7,000 (or $8,000 catch-up) to a traditional IRA.

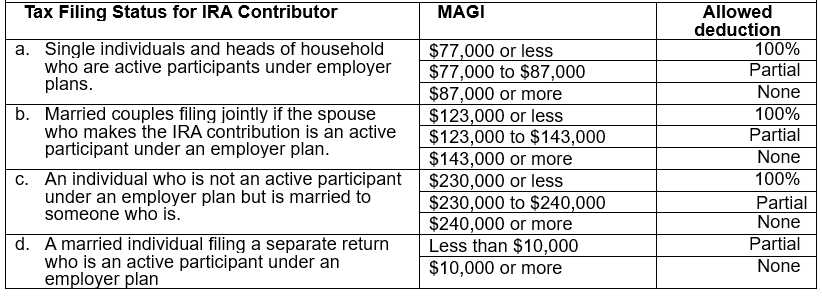

Key Consideration: Deductibility vs. Nondeductibility for Traditional IRA Contributions

An individual can claim a full deduction for a traditional IRA contribution if they are not an active participant in an employer-provided retirement plan nor married to someone who is. They may also be able to claim a deduction if they are an active participant in an employer plan or married to someone who is, and their MAGI is below a certain amount determined by their tax-filing status.

The following is a snapshot of these amounts and the corresponding deductibility rate:

2024 MAGI Limits for Deducting Contributions to Traditional IRAs

An individual who is eligible to claim a deduction for a traditional IRA contribution may treat it as nondeductible for various reasons. And because Roth IRAs are funded with amounts that have already been taxed, it is often recommended that the traditional IRA contribution be treated as nondeductible even if the individual is eligible to deduct the contribution. However, treating a deductible contribution as nondeductible is not always ideal for a backdoor Roth IRA contribution. For example, if an IRA owner has only pretax amounts in their traditional IRA, claiming a deduction for the new contribution would avoid the ongoing pro rata rule application for distributions and conversions. See the section “The pro rata Rule for Pretax and Aftertax Balance” below.

The Backdoor Steps to a Roth IRA

A backdoor Roth IRA contribution is accomplished by making a regular contribution to a traditional IRA and then converting the amount (or a portion of it) to a Roth IRA.

The traditional IRA contribution must be made by the individual’s tax-filing due date. Extensions do not apply. For example, a 2024 IRA contribution must be made by April 15, 2025.

The conversion step has no deadline. However, it should be done immediately after the contribution to ensure that the contribution’s gains accrue in the Roth IRA where it could eventually become tax-free. See Is Your Roth IRA Distribution Taxable? and Answers to Your Roth IRA Questions.

The Pro Rata Rule for Pretax and Aftertax Balance

If you have pretax amounts in your traditional IRA, the conversion will include a prorated amount of pretax and aftertax amounts.

Example:

Charles has a traditional IRA balance of $95,000, all of which is pretax.

Charles made a nondeductible traditional IRA contribution of $5,000 in 2024, bringing the total balance to $100,000.

Charles immediately converted the $5,000 to his Roth IRA.

Charles did not take any other distributions or perform any other Roth conversion in 2024.

While the $5,000 is a nondeductible contribution and would be tax-free when distributed or converted from his traditional IRA, a partial (less than $100,000) conversion would include only a portion of it because of the pro rata rule.

Charles’ conversion of $5,000 would include:

- $4,750 taxable amount.

- $250 nontaxable amount.

The remaining $4,750 of the $5,000 nondeductible contribution would remain in Charles’ traditional IRA and eventually come out in the wash for future distributions and Roth conversions.

See How to Make a Tax-Free Donation From Your IRA for a QCD exception to the pro rata rule.

The pretax and aftertax ratio is calculated on IRS Form 8606 and factors in any aftertax accrued in previous years.

Aggregation of IRAs for Basis Purposes and the Need to File Form 8606

When calculating the aftertax amount included in a Roth conversion, all of your traditional IRAs, SEP IRAs, and SIMPLE IRAs are aggregated and treated as one traditional IRA.

IRS Form 8606 tracks your IRA’s aftertax (basis) amount to prevent double taxation on such amounts. This includes reporting a nondeductible contribution to your traditional IRA, taking a distribution when you have basis in your traditional IRA, and performing a Roth conversion.

Failure to file IRS form 8606 when it is required could result in double taxation. Additionally, the IRS might assess a $50 penalty for failure to file and a $100 penalty if you overstate your nondeductible contributions.

Rollover to Employer Plan To Avoid Pro Rata Treatment

An individual who participates in an employer plan—such as a defined-contribution plan—can roll over their pretax balance from their traditional IRA to that plan. However, such a rollover is permitted only if the plan is designated to accept rollovers from the IRA.

Using Charles’ example above, if he participates in a 401(k) plan that accepts rollovers from traditional IRAs, he could roll over the $95,000 to his 401(k) plan. That would leave only the $5,000 contribution, allowing for a complete tax-free conversion of the $5,000—no pro rata rule.

Individuals who want to use this strategy should check with their employer to see whether the plan is designed to accept rollovers from IRAs and whether there are any restrictions.

Reminders: A rollover from an IRA to an employer plan cannot include aftertax amounts, and any required minimum distribution due for the year must be taken before the rollover. For this strategy to work, Charles must not roll over any amounts from his employer plan to a traditional IRA in 2024.

The IRA Owner’s Tax Advisor Must Be Informed

A backdoor Roth IRA contribution must be reported on the IRA owner’s tax return. To that end, their tax preparer must be notified of the contribution to the traditional IRA and when the conversion was done so that the proper tax reporting is reflected on the client’s tax return.

IRS Form 1099-R—which would report the conversion from the traditional IRA to the Roth IRA—is usually issued by Jan. 31 of the following year, and a copy must be provided to the tax preparer. Form 5498 for the contribution to the traditional IRA and the conversion to the Roth IRA would not be issued until May of the following year. Therefore, the tax preparer should be provided with copies of the regular account statements that include those transactions, as the information can be used for the tax return.

Denise will discuss the final RMD regulations during a preconference session at the NAPFA Fall 2024 conference and key Roth IRA rules during a breakout session. Register here.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

Denise Appleby is a freelance writer. The opinions expressed here are the author’s. Morningstar values diversity of thought and publishes a broad range of viewpoints.

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/EM5S5PPZOBAPZAXTPIQY2RBDYI.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/F4LLDEXKHBDARJDJB7US5S66YU.png)

/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GMMWQCGBLBHCNCOH6F52MYB57A.png)